Foreclosures are at an all time high, real estate markets are slowing down, interest rates are going up, and homeowners are starting to panic about not being able to make their mortgage payments. Foreclosure homeowners are distressed. You prioritized your spending and saved enough money for a small down payment. If you don’t file an answer to the lawsuit, you’ll automatically lose the case and the court will issue the lender a default judgment permitting it to proceed with a foreclosure sale.

Foreclosures are at an all time high, real estate markets are slowing down, interest rates are going up, and homeowners are starting to panic about not being able to make their mortgage payments. Foreclosure homeowners are distressed. You prioritized your spending and saved enough money for a small down payment. If you don’t file an answer to the lawsuit, you’ll automatically lose the case and the court will issue the lender a default judgment permitting it to proceed with a foreclosure sale.

Recovery from the devastating affects of foreclosure is the second step for homeowners. Foreclosure is a situation in which a homeowner is unable to make mortgage payments as required, which allows the lender to seize the property, evict the homeowner and sell the home, as stipulated in the mortgage contract.

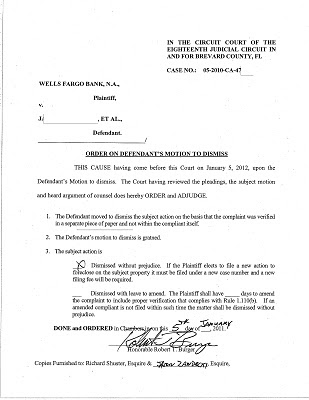

A judicial foreclosure involves going through a court and allows the homeowner to contest the foreclosure. At this point, if the borrower cannot pay, the lender may file a Notice of Foreclosure, which begins the process. Well, is it possible that the lender through its attorney is possibly committing fraud on the court by stating that “the original note is lost” when in fact it cannot be lost, IF the mortgage company sold it.

Most first time home buyers or investors do not have thousands of dollars saved for a down payment on a house. You will have to make payments for the bankruptcy and continue to pay all existing payments on time. A. Out-of-court foreclosure proceedings can be processed within two months, although they can vary from state to state.

Generally, a few weeks to a few months after the foreclosure is filed, the sheriff sale will be conducted at the county courthouse. Loan modification (or loan mod)—An agreement between a lender and a homeowner to change the payment terms of a note and mortgage (particularly lowering the interest rate), used to settle a pending foreclosure case.