A foreclosed home is one in which the home owner was unable to pay his home loan so that the lender took over home ownership through the foreclosure process. You own your property until the title goes to a new owner, usually the foreclosing lender, as a result of a foreclosure sale. If you are unable to make your mortgage payment or have already missed one payment, call your lender NOW. A lien is usually held as security for payment of a debt.

A foreclosed home is one in which the home owner was unable to pay his home loan so that the lender took over home ownership through the foreclosure process. You own your property until the title goes to a new owner, usually the foreclosing lender, as a result of a foreclosure sale. If you are unable to make your mortgage payment or have already missed one payment, call your lender NOW. A lien is usually held as security for payment of a debt.

Once the locks have been changed and the homeowners are shut out of the house, but before the foreclosure auction has been conducted, they can try to get access back to the house by calling the local sheriff’s department or the courts. At auction, an opening bid on the property is set by the foreclosing lender.

Also known as a trustee sale, the auction is open to the public and will often take place on the steps of the county courthouse, in a conference room or convention center, or even online. To redeem the property the borrower must pay the amount bid at the sheriff sale plus interest and fees.

Filing bankruptcy automatically stops the foreclosure process. However, they can request the court to secure the property temporarily, which might mean changing the locks on an apparently-abandoned house. You have to be able to make the payments. The law requires your mortgage company and other creditors to work in good faith with you to formulate a reasonable repayment plan so you can get back on track.

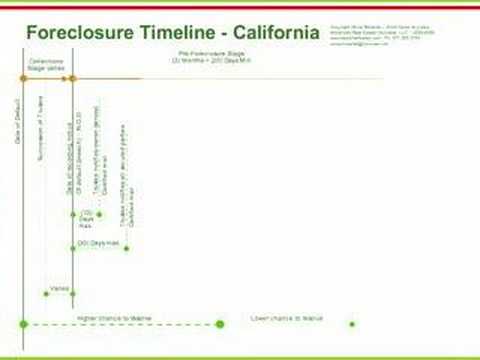

The foreclosure sale (also referred to as the foreclosure auctionâ€) is when the mortgage company sells the property secured by the mortgage loan. 21 days before sale date – The notice of sale must be posted at three public places and mailed to the appropriate parties.